|

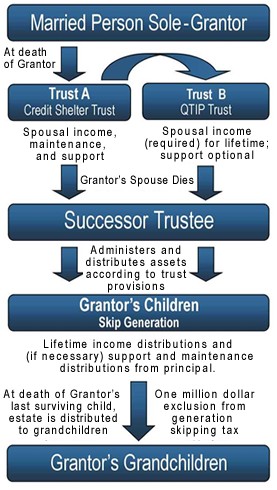

The Married Person Generation Skipping Tax (GST) RLT provides the benefits of a Married Person QTIP Trust and additional features.

|

|

It is a Sole-Grantor trust designed for a married individual wishing to make distributions of principal to skip persons.

|

|

A transfer to a skip person means that no transfer tax was levied on the death of the first generation person; therefore, an additional (GST) tax is levied on such transfers.

|

|

A generation who should have paid transfer tax was skipped by the original transferor so an additional tax (GST) to the transferors estate will be levied.

|

|

The generation skipping tax is an additional tax (additional to estate tax). on assets transferred to skip persons.

|

|

The grantor/transferor is allowed a $1,000,000 exclusion from GST taxes as indexed.

|

|

A GST Trust is for the grantor who wishes to provide a means of support to his spouse and/or children but wants the outright distributions to ultimately go to his grandchildren (or even great-grandchildren and beyond).

|

|

All the principal that would go to the skip persons may be used for the lifetime benefit of the grantors children and/or spouse.

|